文字のサイズ

- 小

- 中

- 大

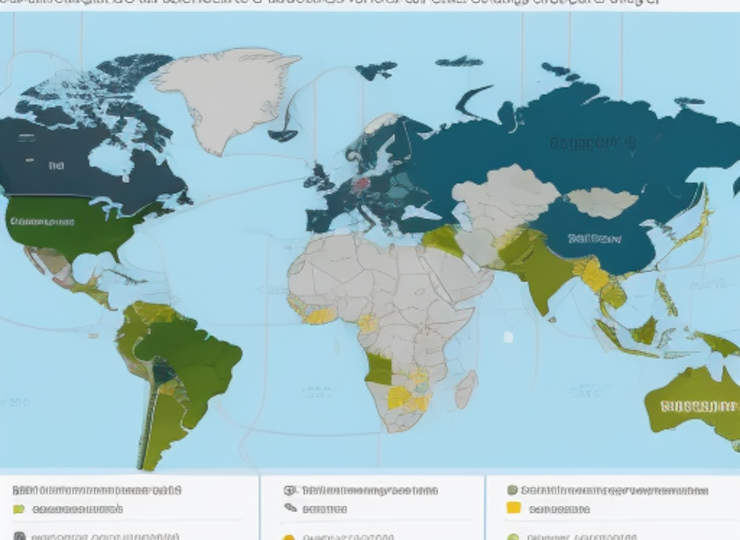

Global electric vehicle sales and EV charging infrastructure

Sales of PEV (BEV/PHEV) passenger cars (including SUVs and other vehicles) in 45 countries grew by 34.6% year-on-year to 12.44 million units in 2023.

Although growth slowed from 2021 (+2.1 times) and 2022 (+52.2%), the market size exceeded 12 million units for the first time, maintaining the expansion trend. In passenger car (including internal combustion engine vehicles) sales, the ratio of passenger cars to the Chinese PEV market, which accounts for more than 50% of the global total, has increased by 7.7 percentage points to 33.2%, in particular to more than 30%, making it clear that China is leading the world as a whole. Outside of China, the ratio of passenger cars to the market in Western Europe is high at 25.2%, while the USA (9.1%), South Korea (8.1%) and Japan (3.5%) are below 10%, indicating that the scale of sales is uneven.

The growth of the PEV market has been driven by two factors: (i) government policies and regulations and (ii) early adopters, but the growth rate has recently shown a slowing trend. The reduction in government incentive measures, exemplified by the slowdown in purchases due to the removal of subsidies in Germany, and the fact that early adopters have run their course can be said to be the factors behind this. Initially, many countries launched BEV promotion measures based on the keyword ‘environment’, but as of June 2024, issues such as the procurement of raw materials for batteries and recycling have become a challenge, and it is beginning to be said that it is necessary to re-examine to what extent these measures will lead to environmental measures.

Some countries (EU/UK, Canada, some states in the US, etc.) have proposed a ban on the sale of internal combustion engine vehicles in 2035, and if these regulations are truly introduced in each country, the BEV market (including some PHEVs in North America) will grow significantly and the PEV market will grow to 40 million units by 2035. However, given the current level of technology, production costs, sales prices and convenience, sales of internal combustion engine vehicles may still be maintained in 2035, with the US presidential election coming up in November 2024, when former President Trump, who is negative towards stricter environmental regulations, is expected to run for president. In Western Europe, too, the future of the PEV market is becoming increasingly difficult to foresee, with discussions on how medium- and long-term policies should be implemented as subsidies are abolished or reduced in earnest.

Meanwhile, the development of EV charging infrastructure networks, which are essential for the spread of electric vehicles, is progressing rapidly: in 2023, the number of EV charging infrastructure units worldwide increased by 44.4% year-on-year to 3.9 million, with the number of units per 10,000 people increasing to 4.9 (2022: 3.4). in the 27 EU countries, the number of EVs increased by 38.0% year-on-year to 592,000. It has been pointed out that the pace of charging network expansion has not kept pace with the expansion of the PEV market, but in recent years the pace of expansion of public charging infrastructure has been greater than the growth in PEV sales (2023: +17.7% y/y). However, there is still a large gap in infrastructure development between countries, which has traditionally been an issue, with the top three countries (the Netherlands, France and Germany) accounting for 60% of the public charging infrastructure in the EU.